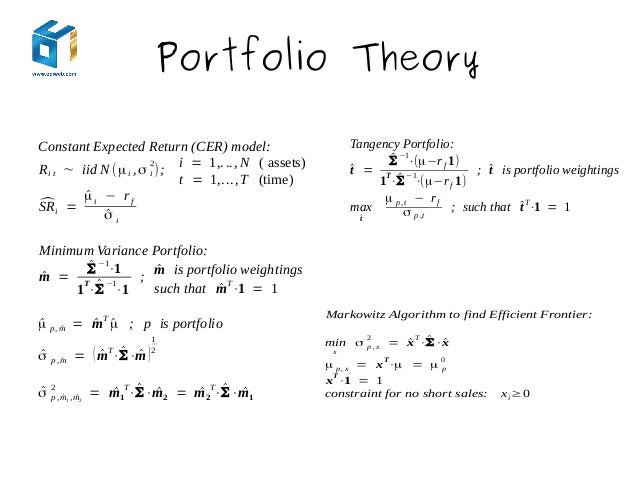

Portfolio Expected Return Formula : Risk & return analysis : Rp = ∑ni=1 wi ri where ∑ni=1 wi = 1 w is the weight of each asset. Allocated_daily_returns = (initial_weight * daily_returns_portfolio_mean) portfolio_return = np.sum (allocated_daily_returns) print (portfolio_return) 0.0010250770900235055 the average daily portfolio return is around 0.1% based on our initial allocation. Risk and return (formulas) rate of return = (amt received − amt invested) / amt invested expected rate of return = p1 r1 + p2 r2 +.pn An abnormal return describes the returns generated by a security or portfolio that differ from the expected return over a specified period. Before markowitz portfolio theory, risk & return concepts are handled by the investors loosely. R p = w 1 r 1 + w 2 r 2 r p = expected return for the portfolio w 1 = proportion of the portfolio invested in asset 1

Mathematically, the portfolio variance formula consisting of two assets is represented as, portfolio variance formula = w12 * ơ12 + w22 * ơ22 + 2 * ρ1,2 * w1 * w2 * ơ1 * ơ2 you are free to use this image on your website, templates etc, please provide us with an attribution link To find out what the excess returns are, jason must first compute the stock's expected return following the capital asset pricing model and then find the excess returns. For a portfolio, you will calculate expected return based on the expected rates of return of each individual asset. Expected return expected return of a portfolio is the weighted average return expected from the portfolio. Let's further assume that we expect a stock return of 8% and a bond return of 6% and our allocation is equal in both funds.

Interactive Visualization in Human Time -StampedeCon 2015 from image.slidesharecdn.com He pointed out the way in which the risk of portfolio to an investor. Expected return of portfolio = 0.2 (15%) + 0.5 (10%) + 0.3 (20%) = 3% + 5% + 6% = 14% Rp = ∑ni=1 wi ri where ∑ni=1 wi = 1 w is the weight of each asset This helps in determining the risk of an investment vis a vis the expected return. For a portfolio, you will calculate expected return based on the expected rates of return of each individual asset. Expected return expected return of a portfolio is the weighted average return expected from the portfolio. Mathematically, the portfolio variance formula consisting of two assets is represented as, portfolio variance formula = w12 * ơ12 + w22 * ơ22 + 2 * ρ1,2 * w1 * w2 * ơ1 * ơ2 you are free to use this image on your website, templates etc, please provide us with an attribution link It is calculated by multiplying expected return of each individual asset with its percentage in the portfolio and the summing all the component expected returns.

The capm formula is used for calculating the expected returns of an asset.

Calculating portfolio return should be an important step in every investor's routine. Expected rate of return (err)= r1 x w1 + r2 x w2 … To calculate expected rate of return, you multiply the expected rate of return for each asset by that asset's weight as part of the portfolio. Expected return of portfolio = 0.2 (15%) + 0.5 (10%) + 0.3 (20%) = 3% + 5% + 6% = 14% E (rp) = w1e (r1) + w2e (r2) where w1, w2 are the respective weights for the two assets, and e (r1), e (r2) are the respective expected returns. Expected return = risk free rate + beta * market return premium = 3.5% + 1.5 * 8.5% = 16.25%. To find out what the excess returns are, jason must first compute the stock's expected return following the capital asset pricing model and then find the excess returns. The expected portfolio is closest to: The formula of expected return for an investment with various probable returns can be calculated as a weighted average of all possible returns which is represented as below, expected return = (p1 * r1) + (p2 * r2) + ………… + (pn * rn) p i = probability of each return r i = rate of return with different probability. This leverages the risk of each individual asset with an offsetting investment, thus hedging the total portfolio risk for the level of risk accepted with respect to the expected rate of portfolio return. The expected return can be calculated as: This lesson will discuss the technical formulas in calculating portfolio return with practical tips for retail investors. This helps in determining the risk of an investment vis a vis the expected return.

Written as a formula, we get: You then add each of those results together. Rp = ∑ (wi * ri) where i = 1,2,3,…….n wi: View fm formula sheet (1).pdf from ee 306 at nixa high school. For a portfolio, you will calculate expected return based on the expected rates of return of each individual asset.

Standard Risk Measure Methodology | Rest Super from www.rest.com.au This lesson will discuss the technical formulas in calculating portfolio return with practical tips for retail investors. To calculate the expected return on an investment portfolio, use the following formula: Portfolio standard deviation is calculated based on the standard deviation of returns of each asset in the portfolio, the proportion of each asset in the overall portfolio i.e., their respective weights in the total portfolio, and also the correlation between. Portfolio expected return is the sum of each product of individual asset's expected return with its associated weight. More how to use the sharpe ratio to analyze portfolio. View fm formula sheet (1).pdf from ee 306 at nixa high school. Rp = ∑ni=1 wi ri where ∑ni=1 wi = 1 w is the weight of each asset Risk and return (formulas) rate of return = (amt received − amt invested) / amt invested expected rate of return = p1 r1 + p2 r2 +.pn

E (rp) = w1e (r1) + w2e (r2) where w1, w2 are the respective weights for the two assets, and e (r1), e (r2) are the respective expected returns.

View fm formula sheet (1).pdf from ee 306 at nixa high school. To calculate the expected return on an investment portfolio, use the following formula: This leverages the risk of each individual asset with an offsetting investment, thus hedging the total portfolio risk for the level of risk accepted with respect to the expected rate of portfolio return. You then add each of those results together. The capm formula is used for calculating the expected returns of an asset. For a portfolio, you will calculate expected return based on the expected rates of return of each individual asset. Portfolio variance is a measure of dispersion of returns of a portfolio. Expected return formula expected return can be defined as the probable return for a portfolio held by investors based on past returns or it can also be defined as an expected value of the portfolio based on probability distribution of probable returns. Let's further assume that we expect a stock return of 8% and a bond return of 6% and our allocation is equal in both funds. Expected return of portfolio = 0.2 (15%) + 0.5 (10%) + 0.3 (20%) = 3% + 5% + 6% = 14% The investors knew that diversification is best for making investments but markowitz formally built the quantified concept of diversification. An investment that is on track to earn its expected return. R p = w 1 r 1 + w 2 r 2 r p = expected return for the portfolio w 1 = proportion of the portfolio invested in asset 1

The investors knew that diversification is best for making investments but markowitz formally built the quantified concept of diversification. An abnormal return describes the returns generated by a security or portfolio that differ from the expected return over a specified period. More how to use the sharpe ratio to analyze portfolio. The expected return can be calculated as: This lesson will discuss the technical formulas in calculating portfolio return with practical tips for retail investors.

Solved: 4. Portfolio Expected Return. We Can Use The Equat ... from d2vlcm61l7u1fs.cloudfront.net Expected return expected return of a portfolio is the weighted average return expected from the portfolio. An investment that is on track to earn its expected return. The expected return of a portfolio is equal to the weighted average of the returns on individual assets in the portfolio. Based on the respective investments in each component asset, the portfolio's expected return can be calculated as follows: But expected rate of return is an inherently uncertain figure. You then add each of those results together. To calculate expected rate of return, you multiply the expected rate of return for each asset by that asset's weight as part of the portfolio. Before markowitz portfolio theory, risk & return concepts are handled by the investors loosely.

The portfolio variance formula is used widely in the modern portfolio theory.

Put simply each investment in a minimum variance portfolio is risky if traded. Expected return formula expected return can be defined as the probable return for a portfolio held by investors based on past returns or it can also be defined as an expected value of the portfolio based on probability distribution of probable returns. To calculate expected rate of return, you multiply the expected rate of return for each asset by that asset's weight as part of the portfolio. To find out what the excess returns are, jason must first compute the stock's expected return following the capital asset pricing model and then find the excess returns. Assume we have a simple portfolio of two mutual funds, one invested in bonds and the other invested in stocks. Rp = ∑ni=1 wi ri where ∑ni=1 wi = 1 w is the weight of each asset The investors knew that diversification is best for making investments but markowitz formally built the quantified concept of diversification. E (rp) = w1e (r1) + w2e (r2) where w1, w2 are the respective weights for the two assets, and e (r1), e (r2) are the respective expected returns. Before markowitz portfolio theory, risk & return concepts are handled by the investors loosely. Written as a formula, we get: Let's further assume that we expect a stock return of 8% and a bond return of 6% and our allocation is equal in both funds. Portfolio variance is a measure of dispersion of returns of a portfolio. The expected return can be calculated as:

Belum ada Komentar untuk "Portfolio Expected Return Formula : Risk & return analysis : Rp = ∑ni=1 wi ri where ∑ni=1 wi = 1 w is the weight of each asset"

Belum ada Komentar untuk "Portfolio Expected Return Formula : Risk & return analysis : Rp = ∑ni=1 wi ri where ∑ni=1 wi = 1 w is the weight of each asset"

Posting Komentar